Triglav increases its operating result and business volume while maintaining strong capitalisation

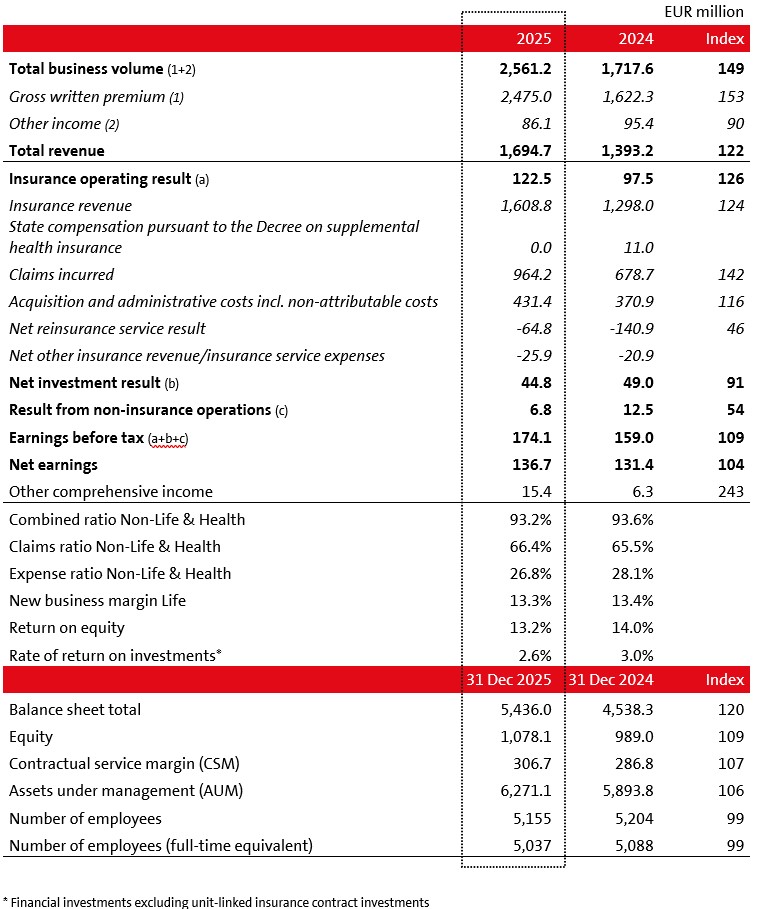

- Compared to 2024, the Group's total business volume grew organically by 9% to EUR 1,868.3 million. Including the new business from the Italian market, the total business volume amounted to EUR 2,561.2 million (49% growth). Organic growth was achieved across all business segments.

- Earnings before tax rose by 9% to EUR 174.1 million, while net earnings increased by 4% to EUR 136.7 million.

- The combined ratio Non-Life and Health stood at a favourable 93.2% (2024: 93.6%), while the new business margin Life stood at 13.3% (2024: 13.4%). The return on equity was 13.2% (2024: 14.0%).

- Capital adequacy at year-end remained within the target range of 200–250%. As at 31 December 2025, Triglav's market capitalisation reached EUR 1.3 billion, the dividend yield was 4.7% and total share return stood at 50.9%.

- For 2026, the Group plans earnings before tax of EUR 170–190 million, with a total business volume exceeding EUR 2.4 billion, and the combined ratio Non-Life and Health of around 95%.

Andrej Slapar, President of the Management Board of Zavarovalnica Triglav, commented: "We are very pleased with the 2025 business results. Profitability was achieved in both the insurance and asset management segments, generating a high operating result. A 9% organic growth in business volume was achieved, while profitability was maintained or improved. Aligned with our ambitious strategy to 2030, we are continuing to diversify operations, further strengthening the Group's resilience. Accordingly, in 2025 the share of business outside Slovenia increased: in the wider international environment, growth and profitability were recorded in reinsurance markets, while in insurance markets a significant business volume from the Italian market was added to the portfolio. Looking ahead, annual volatility in business volume on international markets is expected, while still recognising that insurance operations continue to provide investment opportunities. Consistent with premium growth, claims increased in the past year, which were effectively managed through prudent reinsurance protection, with no major CAT claims recorded. Our business model remains balanced and robust, our capitalisation is at target level, and our financial stability is confirmed by high credit ratings. Investments continue in development, digitalisation and sustainable operations, further reinforcing the dominant position in the region. We are moving forward with confidence, fully focused on creating long-term value for our stakeholders. On behalf of the Management Board, I would like to extend our sincere gratitude to all our Triglav employees for realising our ambitions."

PERFORMANCE HIGHLIGHTS IN 2025 (unaudited)

The Group achieved 9% organic growth in the total business volume, reaching EUR 1,868.3 million. In mid-2025, in cooperation with partners, the Group entered the Italian motor vehicle insurance market, generating an additional EUR 692.9 million in written premium and bringing total business volume to EUR 2,561.2 million (49% growth). Gross written insurance, coinsurance and reinsurance premiums grew by 53% to EUR 2,475.0 million; excluding the new premium from the Italian market, premium growth stood at 10%.

Organic growth was achieved across all business segments. The highest growth, 63%, was recorded in the Non-Life segment, which also contributed the largest share, 83%, of the Group's total business volume (EUR 2,093.5 million).

In line with strategic ambitions, the Group strengthened its business volume outside Slovenia. In the total business volume, the share of the Slovenian market decreased to 40% (2024: 58%), while the business volume on this market grew by 3% to EUR 1,015.4 million. The share of other Adria region markets in the total business volume was 15%, with the business volume increasing by 7% to EUR 374.3 million. The Group generated 46% of the total business volume in international markets (2024: 22%), amounting to EUR 1,171.5 million. On international reinsurance markets, the total business volume increased by 29% to EUR 346.0 million. On international insurance markets, where operations are conducted in partnership (Italy, Poland, Greece, Germany and others), EUR 825.5 million was generated, of which 84% was in the Italian market.

The Group's earnings before tax rose by 9% to EUR 174.1 million year-on-year, while net earnings increased by 4%, reaching EUR 136.7 million. The Group operated profitably in all segments except the Health segment. The majority of earnings before tax, EUR 122.5 million, was generated by the insurance business (2024: 97.5 million), driven primarily by strong performance in the Non-Life segment. Earnings before tax from the investment business totalled EUR 44.8 million (2024: EUR 49.0 million), while EUR 6.8 million was generated from non-insurance operations (2024: EUR 12.5 million). Zavarovalnica Triglav, the Group's parent company, generated earnings before tax of EUR 142.1 million (21% growth). This result was positively affected by the reversal of the impairment of investments in subsidiaries in the amount of EUR 18.0 million, which had no impact on the Group's earnings. The parent company's net earnings amounted to EUR 113.6 million (16% growth).

Other comprehensive income amounted to EUR 15.4 million (2024: EUR 6.3 million), with the increase mainly resulting from the effect of rising risk-free interest rates on the revaluation of investments and liabilities – higher risk-free interest rates were primarily at the long-term end of the yield curve, where aligning interest rate sensitivity between assets and liabilities is particularly challenging due to the absence of appropriate financial instruments. The Group's capitalisation as at 31 December 2025 was within the target range of 200–250%.

The combined ratio Non-Life and Health stood at a favourable 93.2% (2024: 93.6%). Claims development was favourable. The increase in the claims ratio by 0.9 percentage points to 66.4% was primarily driven by the increased structural growth in the international insurance portfolio. The expense ratio decreased by 1.3 percentage points to 26.8%, as the growth in insurance revenue outpaced the growth in expenses. The Group increased its business volume and maintained or improved favourable profitability of the insurance business across all Adria region markets, with the exception of Bosnia and Herzegovina, where ownership consolidation and business optimisation are ongoing. The combined ratio of international insurance and reinsurance stood at 95.3%

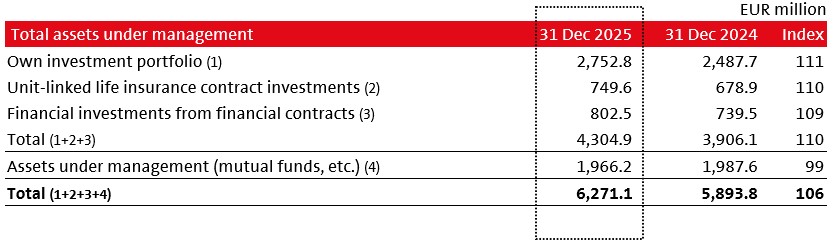

The Group's total assets under management remained broadly unchanged in composition compared to the end of the previous year. Their volume, however, increased by 6% to EUR 6.3 billion. In volatile financial market conditions, the Group achieved a 2.6% rate of return on investments (2024: 3.0%), excluding unit-linked insurance assets. The rate of return is largely comparable to last year's, excluding the effect of exchange rate differences on investments, which are offset by changes in insurance provisions, and the impact of business growth in the Italian market on the value of financial investments.

TRIGLAV GROUP PERFORMANCE BY SEGMENT

Uroš Ivanc, a Management Board member of Zavarovalnica Triglav, said: "All business segments were profitable, with the exception of the Health segment. Following a revision of its business model in 2024, we expect some volatility in results going forward, until the segment reaches the target business volume. The segment is steadily growing, and we achieved premium growth across all markets. In the Non-Life segment, we delivered a very strong increase in operating results, driven by portfolio growth, improved profitability and the absence of significant CAT events. The Life segment maintained a sound new business margin, increased its business volume and achieved a solid operating result. While the insurance operating result improved, the investment result was lower due to financial market conditions. These market conditions also resulted in a lower year-on-year result from own investments in the Asset Management segment. Nevertheless, we successfully increased income from fees and expanded business volume in this segment."

Non-Life segment

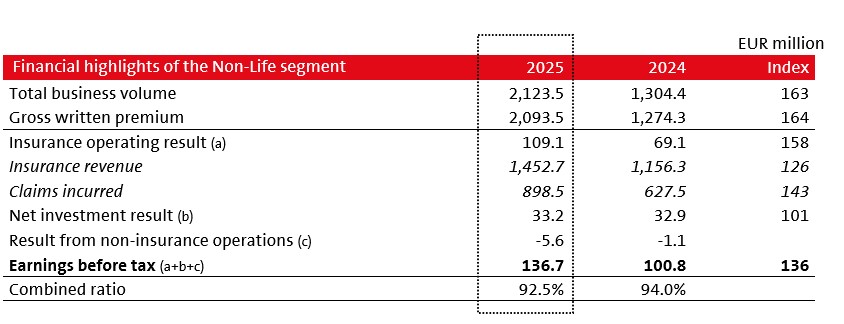

- The total business volume increased by 63% to EUR 2,123.5 million.

- The combined ratio stood at a favourable 92.5% (2024: 94.0%).

- Earnings before tax rose by 36%, reaching EUR 136.7 million.

The total business volume increased by 63%, reaching EUR 2,123.5 million. Gross written premium increased at a similar rate, with growth achieved across most non-life insurance groups. By market, a strong premium growth of 210% was recorded in international markets (with reinsurance premium up 29% and insurance premium up 656%). The largest share of this growth was recorded in the Italian market, followed by Poland and Greece. Premium growth was observed in Slovenia and across all other Adria region markets, with the exception of Bosnia and Herzegovina, where ownership consolidation and business optimisation are ongoing.

The total business volume increased by 63%, reaching EUR 2,123.5 million. Gross written premium increased at a similar rate, with growth achieved across most non-life insurance groups. By market, a strong premium growth of 210% was recorded in international markets (with reinsurance premium up 29% and insurance premium up 656%). The largest share of this growth was recorded in the Italian market, followed by Poland and Greece. Premium growth was observed in Slovenia and across all other Adria region markets, with the exception of Bosnia and Herzegovina, where ownership consolidation and business optimisation are ongoing.

The total business volume increased by 63%, reaching EUR 2,123.5 million. Gross written premium increased at a similar rate, with growth achieved across most non-life insurance groups. By market, a strong premium growth of 210% was recorded in international markets (with reinsurance premium up 29% and insurance premium up 656%). The largest share of this growth was recorded in the Italian market, followed by Poland and Greece. Premium growth was observed in Slovenia and across all other Adria region markets, with the exception of Bosnia and Herzegovina, where ownership consolidation and business optimisation are ongoing.

The total business volume increased by 63%, reaching EUR 2,123.5 million. Gross written premium increased at a similar rate, with growth achieved across most non-life insurance groups. By market, a strong premium growth of 210% was recorded in international markets (with reinsurance premium up 29% and insurance premium up 656%). The largest share of this growth was recorded in the Italian market, followed by Poland and Greece. Premium growth was observed in Slovenia and across all other Adria region markets, with the exception of Bosnia and Herzegovina, where ownership consolidation and business optimisation are ongoing.Non-life insurance claims incurred increased by 43% to EUR 898.5 million. In 2024, claims incurred decreased, and the claims provisions made in 2023 due to the floods were released. In 2025, however, claims incurred increased, primarily driven by the growth of the international insurance portfolio.

The combined ratio Non-Life stood at a favourable 92.5%, down 1.5 percentage points year-on-year, with both the expense ratio and the claims ratio decreasing. The improved ratios reflect revenue growth outpacing expense growth and an improvement in net claims development.

Earnings before tax rose by 36%, reaching EUR 136.7 million. The net investment result remained at last year's level, while the insurance operating result increased significantly. It was mainly driven by higher business volume and improved profitability of the insurance business.

Life segment

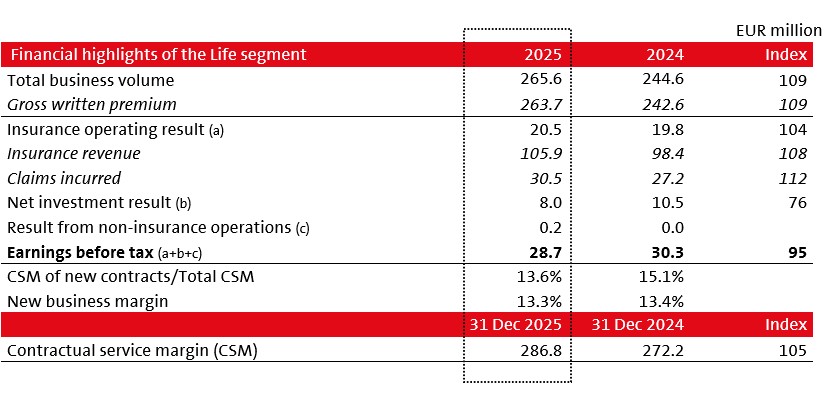

- The total business volume increased by 9% to EUR 265.6 million.

- The new business margin stood at a favourable 13.3% (2024: 13.4%). The contractual service margin increased by 5%, reaching EUR 286.8 million.

- Earnings before tax amounted to EUR 28.7 million (2024: EUR 30.3 million).The total business volume of EUR 265.6 million grew by 9%, as did the life insurance premium. Gross written premium increased across all of the Group's insurance markets. Its growth was particularly strong in unit-linked life insurance, driven by additional premium payments.

The total business volume of EUR 265.6 million grew by 9%, as did the life insurance premium. Gross written premium increased across all of the Group's insurance markets. Its growth was particularly strong in unit-linked life insurance, driven by additional premium payments.

The total business volume of EUR 265.6 million grew by 9%, as did the life insurance premium. Gross written premium increased across all of the Group's insurance markets. Its growth was particularly strong in unit-linked life insurance, driven by additional premium payments.The new business margin stood at a favourable 13.3% (2024: 13.4%).

The contractual service margin of EUR 286.8 million rose by 5%, while the share of the CSM of new contracts in total contractual service margin was 13.6% (2024: 15.1%). The CSM of new contracts amounted to EUR 39.0 million, of which 40% was accounted for by unit-linked life insurance contracts. The release of the contractual service margin to profit or loss amounted to EUR 40.4 million (2024: EUR 36.6 million).

Earnings before tax of the Life segment declined by 5%, reaching EUR 28.7 million.

The insurance operating result increased by 4%, whereas the net investment result decreased by 24%. This was due to financial market conditions, which led to lower growth in equity investments.

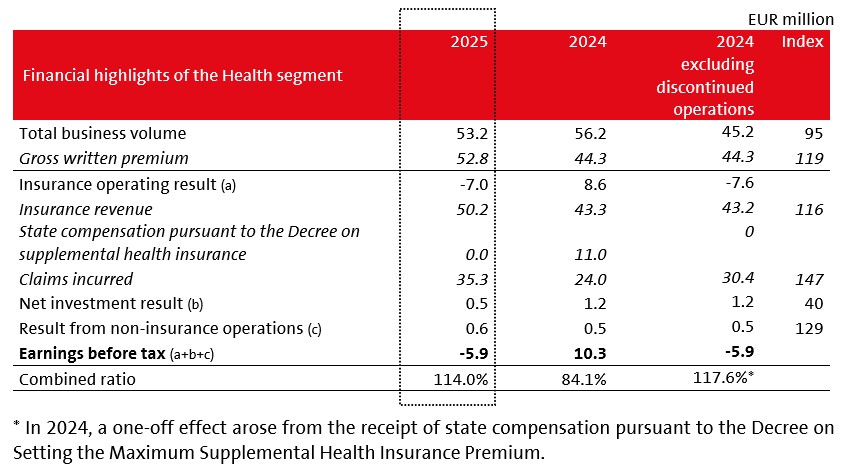

Health segment

- The total business volume amounted to EUR 53.2 million (2024: EUR 56.2 million; including the impact of a one-off event*). Gross written premium increased by 19% to EUR 52.8 million.

- The combined ratio was 114.0% (2024: 84.1.%; or 117.6% excluding a one-off event*).

- Earnings before tax amounted to EUR –5.9 million (2024: EUR 10.3 million*).

Following the restructuring of the segment's business model in 2024, the Group continued activities this year aimed at growing and developing complementary health insurance both in Slovenia and in other regional markets. The Group expects the Health segment's result to remain volatile in the coming period, as the segment is experiencing a phase of strong growth while still maintaining a relatively low business volume.

The segment's total business volume amounted to EUR 53.2 million this year (5% lower than in 2024, which had been higher due to the effect of the termination of supplemental health insurance). Gross written premium amounted to EUR 52.8 million, up 19%. Premium growth was achieved across all markets in the region.

The combined ratio Health stood at 114.0% and improved on a relative basis. In 2024, the ratio stood at 84.1%; however, excluding the impact of supplemental health insurance, it was 117.6%.

Earnings before tax amounted to EUR –5.9 million, compared to EUR 10.3 million year-on-year (of which EUR 16.1 million related to discontinued operations following the termination of supplemental health insurance). The segment recorded a negative result in the insurance business, partly due to higher claims incurred as a result of portfolio growth. The result was positive in the investment business and in non-insurance operations.

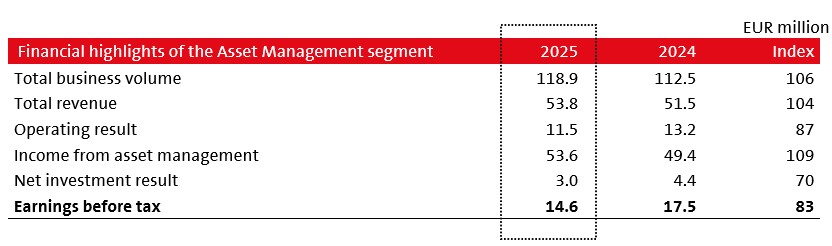

Asset Management segment

- The total business volume increased by 6% to EUR 118.9 million.

- Income from asset management (income from fees) increased by 9% to EUR 53.6 million.

- Earnings before tax declined by 17%, reaching EUR 14.6 million.The total business volume increased by 6%, reaching EUR 118.9 million.

The total business volume increased by 6%, reaching EUR 118.9 million.

The total business volume increased by 6%, reaching EUR 118.9 million.Earnings before tax amounted to EUR 14.6 million (down 17% year-on-year), influenced by a 9% increase in income from asset management (income from fees), which totalled EUR 53.6 million. The net investment result amounted to EUR 3.0 million, down 30%, mainly as a result of a decrease in the value of, or a lower return on, equity investments from the segment's own funds.

Total assets under management, however, increased by 6% to EUR 6.3 billion.

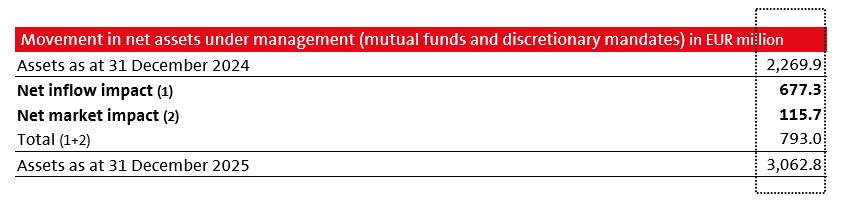

The volume of the Group's assets under management in mutual funds and discretionary mandate assets was positively influenced by both higher client net inflows and financial market conditions. PLAN FOR 2026 AND STRATEGY TO 2030

PLAN FOR 2026 AND STRATEGY TO 2030

(financial highlights)

- Based on currently known and expected business conditions, the Group plans to further increase earnings before tax to between EUR 170 million and EUR 190 million in 2026. The Group's strategic ambition is to double its earnings before tax, relative to the starting point, to EUR 250–300 million by 2030.

- In 2026, the Group plans for the total business volume to exceed EUR 2.4 billion. Its strategic ambition is for the business volume to reach EUR 2.5–3.0 billion by 2030, with assets under management exceeding EUR 10 billion.

- Based on currently known and expected business conditions, the Group estimates that the combined ratio Non-Life and Health will be around 95% in 2026. Its goal is to maintain the combined ratio Non-Life and Health below 95% in the 2025–2030 strategy period and achieve a net return on equity (ROE) of between 12% and 13% by 2030.

- The Group strives to position itself as a stable, safe and profitable investment for investors. It aims to pay out dividends of approximately EUR 400 million to shareholders over the period 2025–2030, in line with its dividend policy, while maintaining its target capital adequacy and ensuring the right conditions for growth and development.